Why Legal Clarity and Cash Settlement Are the Keys to Unlocking Finance’s Future

For more than a decade, blockchain has been hailed as a revolutionary force for capital markets. The promise was seductive: seamless, secure asset transfers without the costly oversight of intermediaries. Faster settlement. 24/7 trading. Lower costs.

Yet, for all the hype, tokenisation has remained largely experimental. That era is ending.

According to a new report by OMFIF and Luxembourg for Finance, Designs for a New Era: Tokenisation Frameworks, the technology is moving from concept to implementation. Regulators, financial institutions, and market infrastructure providers are increasingly aligned: tokenisation can fundamentally change how assets are issued, managed, and exchanged.

But the report also delivers a sobering message. Without legal clarity and a global solution for cash settlement, tokenisation risks remaining a niche experiment rather than the backbone of a new financial system.

The Three Layers of Tokenisation

Not all tokenisation is equal. The report breaks down tokenised assets into three distinct legal categories, each with different implications for investors and issuers:

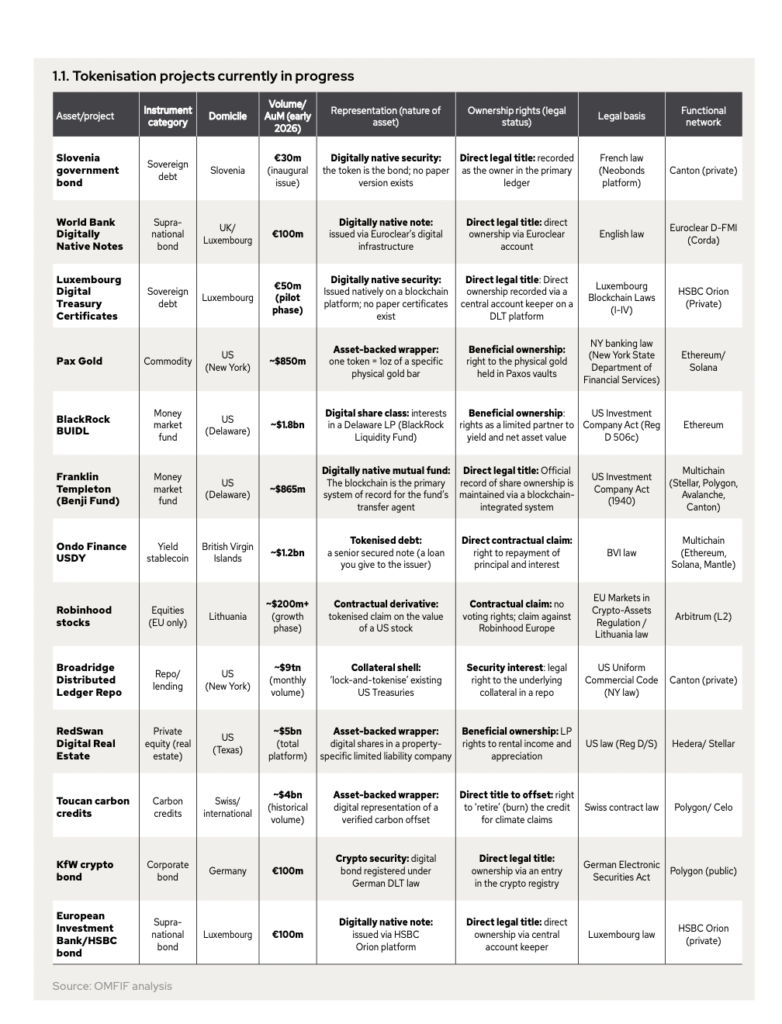

1. Direct tokenisation – The token is the asset. Native digital bonds, such as Luxembourg’s Digital Treasury Certificate, exist purely on-chain. This offers the highest degree of legal certainty.

2. Indirect tokenisation (wrappers) – The token represents a right to an intermediary structure (like a fund or special purpose vehicle) that holds the actual asset. This is common in real-world asset (RWA) tokenisation, where real estate or commodities are packaged into tradeable digital shares.

3. Incomplete tokenisation – The token tracks an asset’s value but confers no legal ownership. Instead, it represents a derivative contract with the issuer. The most prominent example is Robinhood’s stock tokens, which give European investors exposure to US stocks—but make them creditors of Robinhood, not shareholders.

Understanding these distinctions, the authors argue, is critical. “Exactly what a token purporting to represent a financial asset entitles the holder to,” the report states, “is of the first importance.”

The Cash Settlement Conundrum

The single largest obstacle to mainstream tokenisation isn’t technology—it’s money. Early tokenised bond experiments have revealed a hard truth: if you tokenise a security but still settle the cash leg off-chain, you haven’t eliminated settlement risk. You’ve just moved it.

The ideal solution, according to the Bank for International Settlements, is delivery-versus-payment (DVP) in central bank money. Several central banks are moving in this direction. The European Central Bank’s Project Pontes, launching a pilot in late 2026, will offer wholesale central bank digital currency (CBDC) wallets for institutional users, synchronised with tokenised securities platforms. Switzerland is already live with wholesale CBDC on the SDX exchange. But the United States is a glaring exception. Political resistance to CBDCs makes it unlikely the Federal Reserve will issue a tokenised dollar anytime soon. That leaves US markets to rely on private solutions: stablecoins or tokenised commercial bank money.

Stablecoins—particularly regulated ones—are gaining traction as a bridge currency. But banks remain uncomfortable pricing the credit and liquidity risk of stablecoins at scale. Tokenised commercial bank money, like JPMorgan’s Kinexys (formerly JPM Coin), offers a more familiar risk profile, but adoption is still limited to institutional customers. “If a financial instrument is tokenised but there is no equivalent cash facility,” the report warns, “the benefits of tokenising bonds are unlikely to be fully realised.”

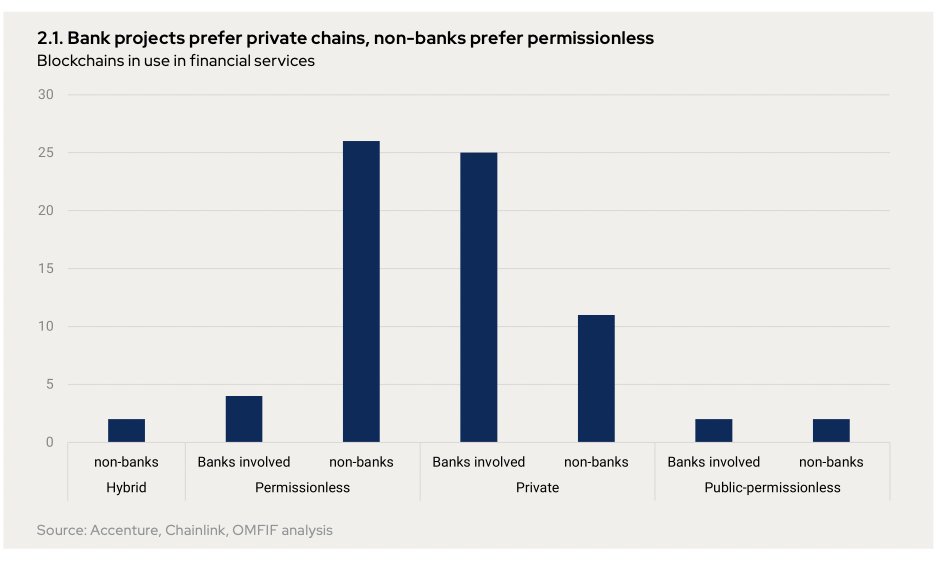

The Blockchain Choice: Public vs. Private

Another fundamental tension is architectural. Public, permissionless blockchains (like Ethereum) offer global reach, deep liquidity, and vibrant developer communities. Private, permissioned chains (run by bank consortia) offer regulatory comfort and clear governance.

The data is stark. According to an analysis by Accenture and Chainlink, banks overwhelmingly prefer private chains for tokenisation projects. Non-banks and fund managers prefer permissionless.

Why? The Basel Committee’s 2022 guidance on cryptoasset exposure assigned a punitive 1,250% capital weighting to assets held on public blockchains—regardless of risk. While the Committee conceded in late 2025 that this must change, the damage is done. Regulators remain uncomfortable with decentralised governance, anonymous validators, and the inability to hold a blockchain directly liable for an outage.

Yet the report points out that these concerns are not insurmountable. Token standards like ERC-3643 already allow only “allow-listed” wallets to hold regulated assets on public chains. And many argue that validators, as neutral parties maintaining network integrity, should not be treated as counterparties at all. “The freedom of movement and the reduction of intermediaries do not imply anarchy,” the report insists. “Financial markets must still be governed by rules.”

Where the Real Transformation Is Happening

Despite the hurdles, tokenisation is already delivering real value in specific corners of finance.

Collateral management is the clearest success story. Broadridge’s distributed ledger repo platform was processing an average of $5.5 billion across 8,542 trades per day as of October 2025. By tokenising collateral, assets remain with their custodian while the record of ownership updates instantly on-chain. This enables intraday repo transactions, meeting margin calls as they arise and lowering the overall collateral required.

Money market funds are also being transformed. Tokenised MMF shares, like BlackRock’s BUIDL (1.8billion ) and 865 million), can be exchanged directly as collateral without first redeeming to cash. Holders continue earning interest, down to minute increments.

Retail access remains a potential game-changer. Fractionalisation—buying a tokenised slice of a $24,000 Berkshire Hathaway share—could democratise investment. But the report cautions that the obstacles to broader retail bond ownership are not technical. They are regulatory and demand-driven. Most large issuers simply don’t need retail investors to meet their funding goals.

The Future: Programmability and Policy Change

Looking further ahead, smart contracts could automate bond lifecycles, payments, and even voting rights. Sustainability-linked bonds could be monitored by IoT sensors, with interest rates adjusting automatically based on real-world environmental data—without the cost of a third-party auditor. But the report’s most important conclusion is about policy. In many cases, the obstacle to unlocking tokenisation is not a technical limitation. It is an outdated rule, a regulatory gap, or a lack of international coordination. “Tokenisation might be a catalyst for policy change,” the authors write. That is the real prize. Not faster settlement for its own sake, but a financial infrastructure that is cheaper, more accessible, and more resilient—built on a foundation of legal certainty, interoperable blockchains, and cash settlement that works across borders and asset classes. The designs for this new era exist. Now comes the hard part: building it.